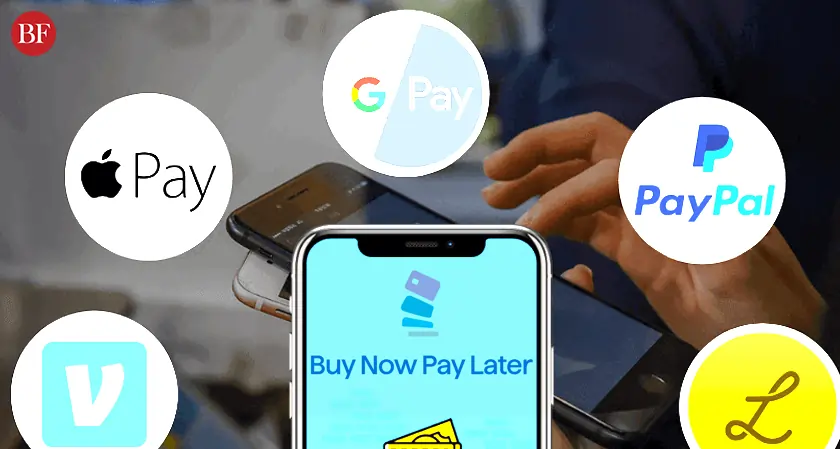

Across India and Southeast Asia, the way people pay, borrow and manage money is changing quickly. Widespread smartphone use, better internet access and a wave of fintech innovation are reshaping everyday financial behavior. Two technologies sit at the center of this shift: digital wallets and Buy Now Pay Later (BNPL) services.

Together, they allow users to make instant payments, access short term credit and complete transactions with just a smartphone. For millions of people, especially younger consumers with limited access to traditional banking or credit cards these tools offer faster and more flexible financial services. At the same time rapid growth has introduced new challenges, including fraud risks and concerns about responsible lending.

Buy Now Pay Later Models

The fast growth of BNPL services in developing countries, particularly India and Southeast Asia, is attributed to the rise of younger mobile savvy consumers and a lack of traditional retail credit. Today BNPL represents over $100 billion worth of e-commerce spending in the Asia Pacific region and demand continues to increase in countries such as Indonesia, Malaysia, Thailand and India.

BNPL is popular mainly because of the ease and rapidity with which requests for BNPL can be made. Many of the leading fintech companies and digital wallets offer their customers the option to apply and obtain approval for a BNPL transaction in less than ten minutes using a digital interface. As a result, BNPL's penetration of the Indian market has increased dramatically: from being a very small share of total e-commerce transactions in 2019 to becoming a well-established payment option over the last several years due in large part to the ability of companies offering this payment option to easily integrate BNPL into the checkout process itself.

However, despite the many benefits associated with having access to BNPL, this payment method does carry risks. BNPL applications often have streamlined application processes creating the risk for consumers of amassing multiple concurrently outstanding BNPL loan products for one person across multiple platforms without proper credit checks. And some studies have found that some illegal providers are linking BNPL products with online gaming sites which raises some concerns about protecting consumers.

Digital Wallets in India and Southeast Asia

Digital wallets have become central to everyday payments across the region. These apps allow users to send money, pay merchants and access financial services directly from their smartphones through phone numbers or QR codes.

In India, the Unified Payments Interface (UPI) has played a major role in expanding digital payments. By connecting bank accounts with mobile apps and enabling instant QR based transactions, UPI has made digital payments widely accessible across both cities and rural communities.

In Southeast Asia, mobile wallets offered by banks and fintech companies are driving rapid growth in e-commerce payments. In markets where credit card usage remains low, many consumers move directly to mobile wallets as their primary financial tool. This trend also supports the expansion of BNPL services since many installment payment options are integrated within wallet platforms.

Strengthening Payment Security

Fraud is a growing concern as digitized payment systems continue to grow because fraudsters target systems using methods including phishing, social engineering and weak authentication to access people's accounts or make transactions. There's been a large increase in fraud involving digital payments in India over the last couple of years, with some amounts being lost being as large as hundreds of crores of rupees. To combat this type of fraud, fintech are focusing on implementing improved security measures.

Some of the technologies used to reduce the amount of fraudulent activity are; multi-factor authentication, biometric verification and using AI to detect unexpected behaviors. The use of tokens is also becoming common to store the payment information securely. However, the preventative measures do not create the same experience for users as traditional forms of payment and could create vulnerability for people that use the payment systems that are easy to get onboard to and require very little verification.

Regulation and Financial Inclusion

To achieve a balance of innovation and user safety, regulators in India and Southeast Asia are developing frameworks for BNPL (buy now pay later) services and digital wallets that both increase access to financial services as well as have clear and appropriate levels of supervision. The Reserve Bank of India introduced Digital Lending Guidelines in India to establish a more transparent and responsible way of lending; these guidelines required all lenders to provide detailed information concerning the loan agreement, check borrowers' backgrounds and have a direct connection with their users instead of trusting solely on the use of a digital application.

Regulatory frameworks are still in development across Southeast Asia. While some regulations exist for improving disclosures and establishing regulatory requirements, there is no consistency between countries, complicating compliance for businesses operating in multiple jurisdictions.

In addition, BNPL providers and digital wallet platforms are required to comply with anti-money laundering regulations, verify the identity of users as well as monitor users in real time for suspicious activity.

The next phase of digital finance

In India and Southeast Asia, consumers are using digital wallets and BNPL (Buy Now, Pay Later) solutions as they shop, pay and access credit. Financial services have changed to be faster and more accessible than ever before for younger consumers who have not been able to utilize traditional bank products.

As the growth of digital wallets continues, so do the challenges of protecting customers, using responsible lending guidelines and creating a clear regulatory framework will be critical to establishing the future of digital finance. If innovation in the fintech industry and regulations move in a parallel direction then this region will likely become one of the most influential digital finance ecosystems in the world.